First Steps

Investment |

|||||

Money earned is partly spent and the rest is saved for meeting future expenses. Instead of keeping the resource(money) idle , it is used to earn a return in the future, this is called investment. |

|||||

Why to invest? |

|||||

To put forward in simple terms we invest in order to create wealth. While investing is relatively painless, its rewards are plentiful. To understand why investment is necessary, we need to realize what we lose when we just save and do not invest. That is because the value of the rupee decreases every year due to inflation. For example, if you ran a household within a budget of Rs.10000 in 2000, to run the same household today (assuming the same set of expenses) you would probably need Rs 15,000. This means Rs15,000 is added to your budget because of inflation. Thus we need to generate an additional Rs15,000 and that can be possible only by INVESTING your hard-earned money. |

|||||

To sum up, we need to invest for the following reasons |

|||||

|

|||||

When to start investing |

|||||

The sooner one starts investing the better. Investing early would allow investments to grow more with time, whereby the concept of compounding increases your income, by accumulating the principal and the interest or dividend earned on it, year after year. |

|||||

The three rules for all investors are |

|||||

|

|||||

How much money do I need to invest? |

|||||

There is no statutory amount that an investor needs to invest inorder to generate adequate returns from his savings. The amount that you invest will eventually depend on factors such as: |

|||||

|

|||||

Options available for investment |

|||||

Physical assets like real estate, gold, commodities etc. |

|||||

AND/OR |

|||||

Financial assets like fixed deposits with banks, small savings instruments with post offices, insurance/provident/pension fund etc. or securities market related instruments like shares, bonds, debentures etc. |

|||||

Twelve important steps to investing |

|||||

|

|||||

Interest |

|||||

Interest is an amount charged to the borrower for the privilege of using the lender’s money. Interest is usually calculated as a percentage of the principal balance (the amount of money borrowed). The percentage rate may be fixed for the life of the loan, or it may be variable, depending on the terms of the loan. |

|||||

Factors which determine the interest rates |

|||||

|

|||||

Short term financial options available for investment |

|||||

Savings bank account |

|||||

is often the first banking product people use, which offers low interest (4%-5% p.a.), making them only marginally better than fixed deposits. |

|||||

Money market or liquid funds |

|||||

are a specialized form of mutual funds that invest in extremely short-term fixed income instruments and thereby provide easy liquidity. Money market funds are primarily oriented towards maximizing returns,protecting capital and usually yield better returns than savings accounts, but lower than bank fixed deposits. |

|||||

Fixed deposits with banks |

|||||

are also referred to as term deposits and minimum investment period for bank FDs is 30 days. Fixed Deposits with banks are for investors with low risk appetite, and may be considered for 6-12 months investment period as normally interest on less than 6 months bank FDs is likely to be lower than money market fund returns. |

|||||

Long term financial options available for investment |

|||||

Post office savings |

|||||

Post Office Monthly Income Scheme is a low risk saving instrument, which can be availed through any post office. It provides an interest rate of 8% per annum, which is paid monthly. Minimum amount, which can be invested, is Rs. 1,000/- and additional investment in multiples of 1,000/-Maximum amount is Rs. 3,00,000/- (if Single) or Rs. 6,00,000/- (if held Jointly) during a year. It has a maturity period of 6 years. Premature withdrawal is permitted if deposit is more than one year old. A deduction of 5% is levied from the principal amount if withdrawn prematurely. |

|||||

Public provident fund |

|||||

A long term savings instrument with a maturity of 15 years and interest payable at 8% per annum compounded annually. A PPF account can be opened through a nationalized bank at anytime during the year and is open all through the year for depositing money. Tax benefits can be availed for the amount invested and interest accrued is tax-free. A withdrawal is permissible every year from the seventh financial year of the date of opening of the account and the amount of withdrawal will be limited to 50% of the balance at credit at the end of the 4th year. |

|||||

Company fixed deposits |

|||||

These are short-term (six months) to medium-term (three to five years) borrowings by companies at a fixed rate of interest which is payable monthly, quarterly, semiannually or annually. They can also be cumulative fixed deposits where the entire principal along with the interest is paid at the end of the loan period. The rate of interest varies between 6-9% per annum for company FDs. The interest received is after deduction of taxes. |

|||||

Bonds |

|||||

It is a fixed income (debt) instrument issued for a period of more than one year with the purpose of raising capital. The central or state government, corporations and similar institutions sell bonds. A bond is generally a promise to repay the principal along with a fixed rate of interest on a specified date, called the Maturity Date. |

|||||

Mutual funds |

|||||

These are funds operated by an investment company which raises money from the public and invests in a group of assets. It is a substitute for those who are unable to invest directly in equities or debt because of resource, time or knowledge constraints. Mutual fund units are issued and redeemed by the Fund Management Company based on the fund's net asset value (NAV), which is determined at the end of each trading session. NAV is calculated as the value of all the shares held by the fund, minus expenses, divided by the number of units issued. Mutual Funds are usually long term investment vehicle though there some categories of mutual funds, such as money market mutual funds which are short term instruments. |

|||||

Need for capital |

|||||

Companies require capital for the following purposes |

|||||

|

|||||

Sources of finance for companies |

|||||

Own Capital – It is the money which the promoters or the owners of the company invest . This is internal source of financing the business. |

|||||

AND/OR |

|||||

External Sources- It is the money which is borrowed from the external sources like raising from banks or other financial institutions or through issue of financial instruments to the public like shares, debentures etc. |

|||||

External sources for long term financing |

|||||

|

|||||

Equity / Stock |

|||||

A share or stock is also known as an equity share as well. The equity share basically represents ownership in the company. When a company needs capital or money to operate, it generates the required funds by selling ownership in the company. Total equity capital of a company is divided into equal units of small denominations, each called a share. For example, in a company the total equity capital of Rs 3,00,00,000 is divided into 30,00,000 units of Rs 10 each. Each such unit of Rs 10 is called a Share. Thus, the company then is said to have 30,00,000 equity shares of Rs 10 each. The holders of such shares are members of the company and have voting rights. |

|||||

Why do companies need to issue shares to public? |

|||||

Most companies are usually started privately by their promoter(s). Promoters’ capital ,borrowings from banks and financial institutions may not be sufficient for setting up or running the business over a long term. So companies invite the public to contribute towards the equity and issue shares to individual investors. A public issue is an offer to the public to subscribe to the share capital of a company. Once this is done, the company allots shares to the applicants as per the prescribed rules and regulations laid down by SEBI. |

|||||

Different kinds of issues |

|||||

Primarily, issues can be classified as a Public, Rights or Preferential issues (also known as private placements). |

|||||

Initial public offering (IPO) |

|||||

When an unlisted company makes either a fresh issue of securities or an offer for sale of its existing securities or both for the first time to the public. This paves way for listing and trading of the issuer’s securities. |

|||||

A follow on public offering (further issue) |

|||||

When an already listed company makes either a fresh issue of securities to the public or an offer for sale to the public, through an offer document. |

|||||

Rights issue |

|||||

When a listed company which proposes to issue fresh securities to its existing shareholders as on a record date. The rights are normally offered in a particular ratio to the number of securities held prior to the issue. This route is best suited for companies who would like to raise capital without diluting stake of its existing shareholders. |

|||||

A preferential issue |

|||||

An issue of shares or of convertible securities by listed companies to a select group of persons under Section 81 of the Companies Act, 1956 which is neither a rights issue nor a public issue. This is a faster way for a company to raise equity capital. The issuer company has to comply with the Companies Act and the requirements contained in the Chapter pertaining to preferential allotment in SEBI guidelines. |

|||||

Issue price |

|||||

The price at which a company's shares are offered initially in the primary market is called as the Issue price. When they begin to be traded, the market price may be above or below the issue price. |

|||||

Market capitalization |

|||||

The market value of a quoted company, which is calculated by multiplying its current share price (market price) by the number of shares in issue is called as market capitalization. E.g. Company X has 100 million shares in issue. The current market price is Rs. 100. The market capitalization of company X is Rs. 10000 million. |

|||||

Types of shares |

|||||

Equity shares |

|||||

An equity share, commonly referred to as ordinary share, represents the form of fractional ownership in a business venture. |

|||||

Rights issue/ rights shares |

|||||

The issue of new securities to existing shareholders at a ratio to those already held, at a price. For e.g. a 2:4 rights issue at Rs. 100, would entitle a shareholder to receive 2 shares for every 4 shares held at a price of Rs. 100/share. |

|||||

Bonus shares |

|||||

Shares issued by the companies to their shareholders free of cost based on the number of shares the shareholder owns. |

|||||

Preference shares |

|||||

Owners of these kind of shares are entitled to a fixed dividend or dividend calculated at a fixed rate to be paid regularly before dividend can be paid in respect of equity share. They also enjoy priority over the equity shareholders in payment of surplus. But in the event of liquidation, their claims rank below the claims of the company’s creditors, bondholders/debenture holders. |

|||||

Cumulative preference shares |

|||||

A type of preference shares on which dividend accumulates if remained unpaid. All arrears of preference dividend have to be paid out before paying dividend on equity shares. |

|||||

Cumulative convertible preference shares |

|||||

A type of preference shares where the dividend payable on the same accumulates, if not paid. After a specified date, these shares will be converted into equity capital of the company. |

|||||

Equity investment |

|||||

Why should one invest in equities? |

|||||

Equities have the potential to increase in value over time. It also provides portfolio with the growth necessary to reach long term investment goals. Research studies have proved that the equities have outperformed most other forms of investments in the long term. Equities are considered the most challenging and the rewarding,when compared to other investment options. Research studies have proved that investments in some shares with a longer tenure of investment have yielded far superior returns than any other investment. |

|||||

Average return on equities in India |

|||||

Since 1990 till date, Indian stock market has returned about 17% to investors on an average in terms of increase in share prices or capital appreciation annually. Besides that on average stocks have paid 1.5% dividend annually. Dividend is a percentage of the face value of a share that a company returns to its shareholders from its annual profits. Compared to most other forms of investments, investing in equity shares offers the highest rate of return, if invested over a longer duration. |

|||||

Factors that influence the price of a stock |

|||||

Broadly there are two factors |

|||||

|

|||||

The stock-specific factor is related to people’s expectations about the company, its future earnings capacity, financial health and management, level of technology and marketing skills. The market specific factor is influenced by the investor’s sentiment towards the stock market as a whole. This factor depends on the environment rather than the performance of any particular company. Events favorable to an economy, political or regulatory environment like high economic growth, friendly budget, stable government etc. can fuel euphoria in the investors, resulting in a boom in the market. On the other hand, unfavorable events like war, economic crisis, communal riots, minority government etc. depress the market irrespective of certain companies performing well. However, the effect of market-specific factor is generally short-term. Despite ups and downs, price of a stock in the long run gets stabilized based on the stock specific factors. |

|||||

Growth stock / value stock |

|||||

Growth stocks |

|||||

Growth Stocks are companies whose potential for growth in sales and earnings are excellent, are growing faster than other companies in the market or other stocks in the same industry. These companies usually pay little or no dividends and instead prefer to reinvest their profits in their business for further expansions. |

|||||

Value stocks |

|||||

Value stock companies are those which may have been beaten down in price because of some bad event, but still has assets to its name like buildings, real estate, inventories, subsidiaries, and so on. Many of these assets still have value, yet that value may not be reflected in the stock's price. Value investors look to buy stocks that are undervalued, and then hold those stocks until the rest of the market realizes the real value of the company's assets. The value investors tend to purchase a company's stock usually based on relationships between the current market price of the company and certain business fundamentals. |

|||||

How can one acquire equity shares? |

|||||

|

|||||

Allotment in case of IPO |

|||||

|

|||||

BID and ASK price |

|||||

The ‘Bid’ is the buyer’s price. It is this price that needs to be known when the stock has to be sold. Bid is the rate/price at which there is a ready buyer for the stock, which seller intends to sell. The ‘Ask’ is the price that needs to be known when stock has to be bought i.e. it is the rate/ price at which there is seller ready to sell his stock. |

|||||

Face value of a share |

|||||

The nominal or stated amount assigned to a security by the issuer is known as the face value of a share.It is the original cost of the share shown on the certificate. It is also known as par value or nominal value.For an equity share, the face value is usually a very small amount (Rs.5 or Rs.10) |

|||||

Market value of a share |

|||||

It is the price at which the share is traded in the stock exchange.The face value doesn’t have much bearing on the price |

|||||

Secondary market |

|||||

Secondary market provides a platform for buying and selling of securities that have already been issued. Stock markets (national and regional) deal in secondary market. One can invest in shares, government securities,derivative products, units of Mutual Funds through secondary market. |

|||||

Portfolio |

|||||

A Portfolio is a combination of different investment assets mixed and matched for the purpose of achieving an investor's goal(s). Items that are considered a part of portfolio can include any asset owned from shares, debentures, bonds, mutual fund units to items such as gold, art and even real estate etc |

|||||

Diversification |

|||||

It is a risk management technique that mixes a wide variety of investments within a portfolio. It is designed to minimize the impact of any one security on overall portfolio performance. Diversification is possibly the best way to reduce the risk in a portfolio. |

|||||

Securities |

|||||

As per Securities Contract (Regulation) Act (SCRA) 1956, securities are Instruments such as shares, bonds, scrips, stocks or other marketable securities of similar nature in or any company, body corporate, government securities, derivatives of securities, units of collective investment scheme, interest and rights in securities, security receipt or any other instruments so declared by the Central Government. The stock exchange where they are dealt with is called security market. |

|||||

Security market |

|||||

Security market is a place where buyers and sellers of securities can enter into transactions to buy and sell shares, bonds, debentures etc. It enables corporates, entrepreneurs to raise resources for their companies and business ventures through public issues. It enables to tansfers resources from those having idle ( investors) to others who have a need for them (corporates) most efficiently. Hence, it links savings to investments through various financial products, called securities |

|||||

Regulators for security market |

|||||

|

|||||

Issue of securities |

|||||

Securities can be issued at face value, premium or discount in domestic and/or international market |

|||||

SEBI |

|||||

It is a regulatory authority which is established under Sec 3 of SEBI Act, 1992. |

|||||

SEBI has statuary powers for |

|||||

|

|||||

SEBI functions |

|||||

|

|||||

ISSUE of securities |

|||||

It can be done at face value, premium or discount. The securities may be issued in domestic and/or international market |

|||||

Stock exchange |

|||||

Formed under Securities Contract (Regulation) Act , 1956. It is a body of individuals constituted for the purpose of assisting, regulating or controlling the business of buying, selling or dealing in securities. |

|||||

Stock exchanges |

|||||

|

|||||

Trading in stock exchanges |

|||||

The traditional method of trading used to take place through open outcry without use of information technology for immediate recording or matching of trades. This was time consuming and inefficient. This imposed limits on trading volumes and efficiency. In order to provide efficiency, liquidity, and transparency, NSE introduced a nation wide, online fully automated screen based trading system where a member can punch into the computer the quantities of a security and the price at which he would like to transact, and the transaction is executed as soon as a matching order from the counter party is found. |

|||||

Investor access to IBT |

|||||

Internet based trading enables an investor to buy/sell securities through internet which can be accessed from a computer at the investor’s residence or anywhere else where the client can access the internet. Investors need to get in touch with the NSE broker providing this service to avail of the internet based trading facility. |

|||||

Demutualization of exchange |

|||||

It refers to the legal structure of the exchange where ownership, management and trading rights are segregated from each other. So, it doesn’t lead to conflict of interest in decision making. In India, NSE and OTCEI ( over the counter exchange of India) are demutualised |

|||||

Demat account |

|||||

It is mandatory for an investor to have a demat account which is managed by a depository. Hence, an investor needs to choose a SEBI registered intermediary who can give guidance regarding the formalities required to be met with. |

|||||

Opening a demat account |

|||||

The investor has to approach a Depository Participant and fill up an account opening form with the support proof of identity and address. |

|||||

|

|||||

Contract note |

|||||

Contract note is a confirmation of trades done on a particular day on behalf of the client by the trading member.It is the only proof that a client has with him of the transactions that have taken place. It imposes a legally enforceable relationship between the client and the trading member with respect to purchase/sale and settlement of trades.It also helps to settle disputes/claims between the investor and the trading member.The contract note should be received from the broker within 24 hours of the transaction. |

|||||

Benefits of trading through a recognized stock exchange |

|||||

|

|||||

Entities in trading system |

|||||

Trading members |

|||||

|

|||||

Clearing members |

|||||

|

|||||

Professional clearing members |

|||||

|

|||||

Participants |

|||||

|

|||||

Order types and condition |

|||||

The system allows the trading members to enter orders with various conditions attached to them as per their requirements. These conditions are broadly divided into the following categories: |

|||||

|

|||||

Time condition |

|||||

|

|||||

Price condition |

|||||

| Stop Loss The facility allows the user to release an order into the system, after the market price of the security reaches or crosses a threshold price e.g. if for a stop loss buy order the trigger is Rs. 1027 the limit price is Rs. 1030 and the market price is Rs. 1023 then the order is released into the system once the market price reaches or crosses Rs. 1027 | |||||

Margins |

|||||

Types of margins |

|||||

|

|||||

Margin call |

|||||

When the margin posted in the margin account is below the minimum margin requirement, the broker or exchange issues a margin call. The investor then closes his position or provides additional margin to keep his position open |

|||||

Depository |

|||||

Two main depositories |

|||||

|

|||||

NSDL |

|||||

|

|||||

CDSL |

|||||

|

|||||

Depository participant |

|||||

A Depository Participant (DP) is described as an agent of the depository. They are the intermediaries between the depository and the investors. The relationship between the DPs and the depository is governed by an agreement made between the two under the Depositories Act, 1996. Legally, a DP is an entity who is registered as such with SEBI under the provisions of the SEBI Act. As per the provisions of the SEBI Act, a DP can offer depository- related services only after obtaining a certificate of registration from SEBI |

|||||

Capital market intermediaries |

|||||

Merchant bankers |

|||||

Mandated by SEBI to overlook Public Issues (as Lead Managers) and open offers in takeovers |

|||||

|

|||||

Underwriting of Shares and debentures |

|||||

Other Services |

|||||

|

|||||

Stock broker |

|||||

Stock brokers are intermediaries who are allowed to trade in securities of the stock exchange they are members of. They buy and sell on their own behalf as well as on the behalf of their clients and charge a commission while trading on behalf of their clients for every transaction that the customer makes. In addition they offer research tips and advise the client on when to buy and when to sell stocks in the market. They also intimate clients as to when new offers and NFO’s come in the market to enable them to trade better in the market. |

|||||

Mutual fund |

|||||

Mutual funds are financial intermediaries which collect savings from a large no. of small investors and then invest these funds in a diversified portfolio (ie a collection of different stocks) to minimize the risk and maximize returns for their participants. |

|||||

Profitability ratios |

|||||

|

|||||

|

|||||

Some of the profitability ratios related to investments are: |

|||||

|

|||||

|

|||||

( Here, Capital Employed = Fixed Assets + Current Assets – Current Liabilities) |

|||||

|

|||||

(Net Worth includes shareholder’s Equity capital plus reserves and surplus) |

|||||

A common (equity) shareholder has only a residual claim on profits and assets of a firm, i.e. ,only after claims of creditors and preference shareholders are fully met, the equity shareholders receive a distribution of profits or assets on liquidation. A measure of his well being is reflected by return on equity. |

|||||

There are several other measures to calculate return on shareholder’s equity: |

|||||

(i) Earnings Per Share (EPS): |

|||||

EPS measures the profit available to the equity shareholders per share, that is, the amount that they can get on every share held. It is calculated by dividing the profits available the profits available to the shareholders by number of outstanding shares. The profits available to the ordinary shareholders are arrived at by net profits after taxes and preference dividend. |

|||||

It indicates the value of equity in the market |

|||||

|

|||||

|

|||||

(iii) Cash Earnings Per Share (CPS/CEPS): |

Derivatives |

||||||||||||||||||||

Financial markets are, by nature, extremely volatile and hence the risk factor is an important concern for financial agents. To reduce this rick, the concept of derivatives comes into the picture. |

||||||||||||||||||||

Derivatives have probably been around for as long as people have been trading with one another. Forward contracting dates back at least to the 12th century, and may well have been around before then. Merchants entered into contracts with one another for future delivery of specified amount of commodities at specified pric. A primary motivation for pre-arranging a buyer or seller for a stock of commodities in early forward contracts was to lessen the possibility that large swings would inhibit marketing the commodity after a harvest. |

||||||||||||||||||||

In short, derivative is not an asset in itself but an agreement or a contract to transfer the real asset in future whenever exercised. The date and price of execution is mentioned in the contract as per agreement between the parties. There are varieties of derivatives available at present like futures, options and swaps; futures and options being the most common ones. They yield better returns with lower capital investment as compared to the amount that will be invested to buy the shares directly form the spot market. |

||||||||||||||||||||

It is governed by the Securities Contract Regulation Act or SCRA 1956. |

||||||||||||||||||||

Development of exchange – traded derivatives |

||||||||||||||||||||

Derivatives have probably been around for as long as people have been trading with one another. Forward contracting dates back at least to the 12th century, and may well have been around before then. Merchants entered into contracts with one another for future delivery of specified amount of commodities at specified price. A primary motivation for pre-arranging a buyer or seller for a stock of commodities in early forward contracts was to lessen the possibility that large swings would inhibit marketing the commodity after a harvest. |

||||||||||||||||||||

The need for a derivatives market |

||||||||||||||||||||

The derivatives market performs a number of economic functions. |

||||||||||||||||||||

|

||||||||||||||||||||

Holder: Holder is the buyer of derivative agreement. By buying an agreement, the buyer may agree to buy or sell the underlying asset. |

||||||||||||||||||||

Seller: One who sells the contract to holder. |

||||||||||||||||||||

Types of derivatives products |

||||||||||||||||||||

Forwards |

||||||||||||||||||||

A forward contract is a customized contract between two entities, where settlement takes place on a specific date in the future at today’s pre- agreed price. |

||||||||||||||||||||

Futures |

||||||||||||||||||||

A future contract is an agreement between two parties to buy or sell an asset a certain time in the future at a certain price. They are different from futures contract as they are standardized by the exchange . |

||||||||||||||||||||

Options |

||||||||||||||||||||

Options are of two types call and put. Call gives the buyer the right but not the obligation to buy a given quantity of the underlying asset at a future date at a pre determined price. Put give the seller the right but not an obligation to sell at a given price at a future date. |

||||||||||||||||||||

Warrants |

||||||||||||||||||||

Options generally have lives upto 1 year, majority of the options trade on the stock market have a maturity of up to 9 months. Longer traded options are called warrants and are generally traded over the counter. |

||||||||||||||||||||

Leaps |

||||||||||||||||||||

These are options having a maturity of up to 3 years. |

||||||||||||||||||||

Basket |

||||||||||||||||||||

Basket options are options on portfolios of underlying assets. The underlying asset is usually a basket of asset. |

||||||||||||||||||||

Swaps |

||||||||||||||||||||

swaps are private agreement between two parties to share cash flows in the future on the basis of a pre determined formula. The two commonly used swaps are: |

||||||||||||||||||||

1. Interest rate swaps: These entail only swapping the interest related cash flows between two parties. |

||||||||||||||||||||

2. Currency swaps: these entail swapping both the principal and the interest rate between the two parties with cash flows in one direction being in a different currency than those in the opposite direction. |

||||||||||||||||||||

Swaptions |

||||||||||||||||||||

Swaptions are options to buy or sell a swap that will become operative at the expiry of the options. Thus a swaption is an option on a forward swap. Rather than have calls and puts, the swaptions market has receiver swaptions and payer swaptions. A receiver swaption is an option to receive fixed and pay floating. A payer swaption is an option to pay fixed and receive floating. |

||||||||||||||||||||

Table 1 The global derivatives industry : outstanding contracts, (in $ billion) |

||||||||||||||||||||

|

||||||||||||||||||||

Source: Bank for International Settlements |

||||||||||||||||||||

(OTC: Over The Counter traded instruments, discussed later.) |

||||||||||||||||||||

Factors driving the growth of financial derivatives |

||||||||||||||||||||

|

||||||||||||||||||||

Table 2 Turnover in derivatives contracts traded on exchanges, (in US$ trillion) |

||||||||||||||||||||

|

||||||||||||||||||||

Basics of futures & options |

||||||||||||||||||||

What are futures and options? |

||||||||||||||||||||

|

||||||||||||||||||||

Futures |

||||||||||||||||||||

In futures contract the buyer and seller enter into an obligatory agreement to exercise the contract at maturity. It is not equity in a stock or commodity. It is a contract – a contract to make or take delivery of a product in the future, at a price set in the present.In formalized trading of futures contracts on exchanges, standardized agreements specify price, quantity and the month of delivery. |

||||||||||||||||||||

Both the buyer and seller have the obligation to exercise the contract which means on maturity, seller will transfer the underlying securities and buyer will make the cash payment as per agreed price. |

||||||||||||||||||||

The buyer does not have to pay any amount for buying a futures contract because it is an enforceable agreement which will get settled on maturity date. |

||||||||||||||||||||

Example of future trading |

||||||||||||||||||||

A person bought a futures contract to buy security A at a price of Rs 500 on a specific future date. On the expiry date, the price went up to Rs 600. So the deal is good for buyer who will get the securities at Rs 100 lesser than the actual market price. On other side, it is devastating for the seller who is obliged to sell them at lower price which has been agreed upon. |

||||||||||||||||||||

Features |

||||||||||||||||||||

Future is again a contract to buy or sell an underlying of a certain qty at a certain future time at a certain price |

||||||||||||||||||||

|

||||||||||||||||||||

Futures terminology |

||||||||||||||||||||

|

||||||||||||||||||||

Options |

||||||||||||||||||||

In options contract the buyer is given an option to decide whether or not he wants to exercise the contract at maturity. |

||||||||||||||||||||

Buyer of the contract has the option to exercise it anytime on or before expiry but seller has the obligation to exercise it. If buyer demands to buy the asset, seller will have to sell it. |

||||||||||||||||||||

Options are two types |

||||||||||||||||||||

|

||||||||||||||||||||

Call option |

||||||||||||||||||||

It gives the buyer, the right to buy the asset at a strike price. A call option is an option to buy a stock at a specific price on or before a Certain date. The seller or writer however has the obligation to sell the asset if the buyer of the call option decides to exercise his option to buy. |

||||||||||||||||||||

Put Option |

||||||||||||||||||||

It gives the buyer a right to sell the asset at the ‘strike price’ to the buyer. Put options are options to sell a stock at a specific price on or before a certain date.The seller or writer however has the obligation to buy the asset if the buyer of the put Option decides to exercise his option to sell. These are like insurance policies. If you buy a new car and they auto insurance on the car, you pay a premium and are hence, protected if the asset is damaged in an accident. If this happens you use your policy to regain the value of the asset. So put options gains in value if the value of the asset decreases. With put option, you can insure a stock by fixing a selling price. If something happens which causes the asset price to fall and thus get damaged, you can exercise your option and sell it at its insured price level. |

||||||||||||||||||||

The buyer has to pay an amount called as Premium for acquiring an additional right of having an option to exercise the contract or not. |

||||||||||||||||||||

Example of option trading |

||||||||||||||||||||

A person bought a call option at a strike price of Rs 100. On maturity the price falls to Rs 80. He will not exercise the contract because he can buy the same asset from the market at Rs 80. However if price rises, he will exercise the contract. Similarly, a person bought a put option at a strike price of Rs 100. On maturity the price shoots up to Rs 150. He will not exercise the contract because he can sell the same asset in the market at Rs 150, rather than giving it to the seller at agreed upon price of Rs 100. |

||||||||||||||||||||

Options terminology |

||||||||||||||||||||

i.e. spot price = strike price |

||||||||||||||||||||

Option payoffs |

||||||||||||||||||||

The profit or loss he makes depends on the spot price of the underlying. If upon expiration the spot price exceeds the strike price he makes a profit. If the strike price is more than the spot price he makes a loss to the amount of premium he has paid. For selling an option the writer of the option charges a premium. If spot price exceeds the strike price the writer starts making losses whereas if the spot price is less than the strike price the option is not exercised and the writer gets a profit of the amount of premium. If the spot price is below the strike price he makes a profit. If the spot price is more than the strike price he leaves his option unexercised and his loss is the amount of premium he has paid. By selling the option the writer of the option gets a premium. The profit or loss that the buyer makes depends on the spot price of the underlying. Whatever is the buyers loss is the sellers gain. |

||||||||||||||||||||

Why do futures and options markets exist? |

||||||||||||||||||||

|

||||||||||||||||||||

Professionals such as grain merchants, energy firms and portfolio managers use futures and options to reduce the risk to their business associated with volatile prices. For example, a flour miller might use a futures contract to set a price now for wheat that he knows he will need to purchase in the future, rather than face the chance that prices could be even higher when he buys the wheat. Similarly, a natural gas producer might use a futures contract to set a price now for gas he will sell in the future, locking in a profit rather than being exposed to the possibility of lower prices. These types of futures and options users are known as hedgers, and are in the market specifically to reduce risk.People who assume risk take it on in exchange for the opportunity for profit. Thus the futures and options markets serve the important function of risk transfer. |

||||||||||||||||||||

Futures and options markets also provide the economy with price discovery. Futures prices are determined by supply and demand. An exchange itself does not set prices; it simply provides a place where buyers and sellers can negotiate. If there are more buyers than sellers, the price goes up. If there are more sellers than buyers, the price goes down. The prices discovered through futures markets offer valuable economic information about supply and demand in a competitive business environment. |

||||||||||||||||||||

How does trading futures and options work? |

||||||||||||||||||||

Similar to stocks, gains and losses are the result of price changes |

||||||||||||||||||||

An added economic benefit of using futures and options markets for many investors is lowered transaction costs. Similar to stocks, gains and losses in futures trading are the result of price changes. If you have sold a futures contract, your trade will show a profit if prices fall. If you have bought, higher prices will produce a profit. To make a profit on a futures trade you can first buy low and then sell high, or reverse the order and sell high, then buy low. |

||||||||||||||||||||

|

||||||||||||||||||||

It is important to understand futures may be highly leveraged. This means that if the price moves in the direction you anticipated you could realize large profits in relation to your initial investment. Conversely, if prices move in the opposite direction of what you anticipated, you could realize large losses in relation to your initial investment. |

||||||||||||||||||||

Options on futures are different from futures themselves in that the most a buyer can lose is the cost of purchasing the option, known as the premium, along with transaction costs. An option seller, however, has unlimited risk. |

||||||||||||||||||||

|

||||||||||||||||||||

|

||||||||||||||||||||

Commodity Derivatives |

||||||||||||||||||||

Futures contracts in pepper, turmeric,gur(jaggery), hessian (jute fabric), jute sacking, castor seed, potato, coffee, cotton, and soybean and its derivatives are traded in 18 commodity exchanges located in various parts of the country. Futures trading in other edible oils, oilseeds and oil cakes have been permitted. Trading in futures in the new commodities, especially in edible oils, is expected to commence in the near future. The sugar industry is exploring the merits of trading sugar futures contracts. The policy initiatives and the modernisation programme include extensive training, structuring a reliable clearinghouse, establishment of a system of warehouse receipts, and the thrust towards the establishment of a national commodity exchange. The Government of India has constituted a committee to explore and evaluate issues pertinent to the establishment and funding of the proposed national commodity exchange for the nationwide trading of commodity futures contracts, and the other institutions and institutional processes such as warehousing and clearinghouses. With commodity futures, delivery is best effected using warehouse receipts(which are like dematerialised securities). Warehousing functions have enabled viable exchanges to augment their strengths in contract design and trading. The viability of the national commodity exchange is predicated on the reliability of the warehousing functions. The programme for establishing a system of warehouse receipts is in progress. The Coffee Futures Exchange India(COFEI) has operated as system of warehouse receipts since 1998. |

||||||||||||||||||||

Exchange-traded vs.OTC(Over The Counter) derivatives markets |

||||||||||||||||||||

The OTC derivatives markets have witnessed rather sharp growth over the last few years, which has accompanied the modernization of commercial and investment banking and globalisation of financial activities. The recent developments in information technology have contributed to a great extent to these developments. While both exchange-traded and OTC derivative contracts offer many benefits, the former have rigid structures compared to the later. It has been widely discussed that the highly leveraged institutions and their OTC derivative positions were the main cause of turbulence in financial markets in 1998. These episodes of turbulence revealed the risks posed to market stability originating in features of OTC derivative instruments and markets. |

||||||||||||||||||||

The OTC derivatives markets have the following features compared to exchange-traded derivatives |

||||||||||||||||||||

|

||||||||||||||||||||

Paricipants in derivatives market |

||||||||||||||||||||

|

||||||||||||||||||||

Hedging |

||||||||||||||||||||

Making an investment to reduce the risk of adverse price movements in an asset. Normally, a hedge consists of taking an offsetting position in a related security, such as a futures contract. An example of a hedge would be if you owned a stock, then sold a futures contract stating that you will sell your stock at a set price, therefore avoiding market fluctuations. Investors use this strategy when they are unsure of what the market will do. A perfect hedge reduces your risk to nothing (except for the cost of the hedge). |

||||||||||||||||||||

The best way to understand hedging is to think of it as insurance. When people decide to hedge, they are insuring themselves against a negative event. This doesn't prevent a negative event from happening, but if it does happen and you're properly hedged, the impact of the event is reduced. So, hedging occurs almost everywhere, and we see it everyday. For example, if you buy house insurance, you are hedging yourself against fires, break-ins or other unforeseen disasters. Portfolio managers, individual investors and corporations use hedging techniques to reduce their exposure to various risks. |

||||||||||||||||||||

In financial markets,hedging against investment risk means strategically using instruments in the market to offset the risk of any adverse price movements. In other words, investors hedge one investment by making another. Technically, to hedge you would invest in two securities with negative correlations. |

||||||||||||||||||||

Hedging cannot help to escape the risk-return tradeoff. A reduction in risk will always mean a reduction in potential profits. Hedging is a technique not to make money but to reduce potential loss. If the investment hedged against makes money, then the profit would be reduced but if the investment loses money and the hedge is successful, it will reduce the loss. |

||||||||||||||||||||

Speculation |

||||||||||||||||||||

Speculation usually involves making assumptions that a particular stock price is going to change. |

||||||||||||||||||||

|

||||||||||||||||||||

Anything can lead to speculation. It can be based on some news or some global reaction. If a company reports consistent growth in net sales the stock price will be worth more and market reaction can drive it more. People may not know each and every product being sold but a close study of a company can give an estimate of where the companies sales are headed. The share value can increase or decrease on a given day due to thousands of reasons. |

||||||||||||||||||||

Why is it present? |

||||||||||||||||||||

Speculation exists because it enhances the functioning of the stock market. The market for stocks itself exists because different people have different views on the same stock. To explain, if all investors had the same view on every company, then everybody would want to buy at the same time or conversely, sell at the same time. The implication is that a market cannot exist because there is simply no one with a different view. |

||||||||||||||||||||

Unlike bank deposits, investing in stocks is, relatively, a risky business. There can be short, sharp fluctuations that result in big gains or losses. One way of looking at speculators is that they are a class of investors who are willing to take more risks on an average. And the thumb rule is that greater the variety (categories of investors), greater the likelihood of trades taking place. |

||||||||||||||||||||

Importance of volume in a market |

||||||||||||||||||||

The biggest advantage of speculation is that it increases the volume of the stocks traded. And volume is absolutely essential in creating a marketplace that functions smoothly. |

||||||||||||||||||||

Higher volume means that investors can enter and exit any moment. Equities are more actively traded than corporate debt in India, thus, providing investors with a handy investment avenue that yield cash at short notice. |

||||||||||||||||||||

Volume also plays an important role in price formation. If there arises a sudden huge sale in any market, the prices will crash. In a stock market that sees sporadic trades, orders for slightly bigger quantities will create huge swings in price. Thus, the price formation will be jerky. |

||||||||||||||||||||

On the other hand, when the market is liquid in terms of frequent trades taking place, the change in price is relatively smooth. Even if big orders come in, the depth in market results in relatively smooth changes taking place. |

||||||||||||||||||||

The downsides |

||||||||||||||||||||

The biggest fear with speculation is that it can accentuate sharp movements. By definition, speculators are the ones who are willing to take bigger risks and are also likely to be first to panic in case of adverse developments. |

||||||||||||||||||||

Arbitraging |

||||||||||||||||||||

"Arbitrage" trading is simply the trading of securities when the opportunity exists during the trading day, to take advantage of differences in value between the markets the trades are made within. Arbitrage trading takes place all day long on most days that the markets are active. |

||||||||||||||||||||

Arbritrage is legally allowed. In fact arbitrage is responsible for a large part of the daily volumes on the NSE & BSE exchanges. What mainly takes place in India is called Market Arbitrage. Market Arbitrage involves purchasing and selling the same security at the same time in different markets (BSE & NSE) to take advantage of a price difference between the two separate markets. In perfect securities markets there would never be any arbitrage traders or trades. Since the securities markets are not perfect when news or other information moves a security or index they can and often do become unequal in price temporally. If the markets were perfect all identical securities would trade at the same value or price on each market they were traded on.A market arbitrageur would short sell the higher priced stock and buy the lower priced one. The profit is the spread between the two assets. |

||||||||||||||||||||

Here is a simple example |

||||||||||||||||||||

Suppose you own 500 shares of RPL. One trading day you notice that RPL is trading at 150 on the BSE and 140 on the NSE. You sell your 600 shares on the BSE at 150 and simultaneously buy back the 600 shares on the NSE at 145. |

||||||||||||||||||||

You profit in this case is 500*10.00 = 5000.00 less brokerages if any. |

||||||||||||||||||||

One of the most popular Arbitrage trading opportunities is played with the S&P futures and the S&P 500 stocks. During most trading days these two will develop disparity in the pricing between the two of them. This happens when the price of the stocks which are mostly traded on the NYSE and NASDAQ markets either get ahead or behind the S&P Futures which are traded in the CME market. Lets say the stocks get ahead of the futures in price. Arbitrage traders will sell the stock and buy the futures. They end up with the same or closely related investment but have just made money by taking the difference in the prices from the two separate markets. |

Commodity

A commodity is a good for which there is demand, but which is supplied without qualitative differentiation across a market. It is a physical substance, such as food, grains, and metals, which is interchangeable with another product of the same type, and which investors buy or sell, usually through futures contracts. The price of the commodity is subject to supply and demand. Risk is actually the reason exchange trading of the basic agricultural products began. Commodities are often substances that come out of the earth and maintain roughly a universal price. A commodity is fungible, that is, equivalent no matter who produces it.

In the broadest sense, a commodity is anything that has value, from watches to time to oranges. In a more specific market sense, however, a commodity is an item which is roughly the same market value across the board, with no difference based on quality.

The mainstream commodity market can be split into a number of different markets: precious metals, industrial metals, livestock, agricultural products, energy, and some commodities that don’t easily fall into a classification. Precious metals include gold, silver, platinum, and palladium. Industrial metals include aluminum, aluminum alloy, nickel, lead, zinc, tin, recycled steel, and copper. Livestock includes live cattle, feeder cattle, pork bellies, and lean hogs. Agricultural products include soybeans, soybean oil, soybean meal, wheat, cotton number two, sugar numbers eleven and fourteen, wheat, corn, oats, rice, cocoa, and coffee. Energy includes ethanol, heating oil, propane, natural gas, WTI crude oil, Brent crude oil, GulfCoast gasoline, RBOB gasoline, and uranium. The commodity market also includes rubber, wool, polypropylene, polyethylene, and palm oil.

Commodity derivatives market

commodity derivatives trade contracts for which the underlying assets is a commodity like, wheat, soyabean, cotton etc or precious metal like Gold and Silver. The commodity derivatives differ from the financial derivatives mainly in the following two aspects: Firstly, due to the bulky nature of the Underlying assets, physical settlement in commodity derivatives creates the need for warehousing. Secondly, in the case of commodities, the quality of the asset underlying a contract can vary largely.

Commodity market in India

India has a long history of future trading in commodities. In India, trading in Commodity future has been existence from the 19th Century with organised trading in Cotton, through the establishment at Bombay Cotton Association Ltd. in 1875. Over a period of time, other commodities were permitted to be traded in future exchanges. Spot trading in India occurs mostly in regional mandis and unorganized market, which are fragmented and isolated.

There were booming activities in this market at one time as many as 100 Unorganized exchanges were conducting forward trade in various commodities. The securities market was a poor competitor of this market as there were not many papers to be traded at that time.

However, many feared that derivatives fuelled unnecessary speculation and were detrimental to the healthy functioning of the market for the underlying commodities. As a result, after independence, commodity option trading and cash settlement of commodity future were banned in 1952.

A further blow come in 1960’s when following several years of several droughts has forced many farmers to default on forward contact and even caused some suicides, forward trading was banned in many commodities considered primary or essential. Consequently, the commodities derivatives market dismantled and remained dormant for about four decades until the new millennium when the Govt. in a complete change in policy, started actively encouraging the commodity derivatives market.

The year 2003 marked the real turning point in the policy frame work for commodity market when the government issued notifications for withdrawing all prohibitions and opening up forward trading in all commodities. This period also witnessed other reforms, such as, amendments to the Essential Commodities Act, Securities (contract) Rules, which have reduced bottlenecks in the development and growth of commodity markets of the country is total GDP, commodities related and dependent industries constitute about roughly 50-60% which itself cannot be ignored.

Why are commodity derivatives required:

India is among the top 5 producer of the most of the commodities in addition to being a major consumer of bullion and energy products. Agriculture contributes more than 23% to be GDP of Indian economy. It employees around 57% of the labour force on a total of 185 million hectares of land. Agriculture sector is an important factor to achieving a GDP growth of 8.10. All this indicates that India can be promoted as a major centre for trading of commodity derivatives.

It is common knowledge that prices of commodities, metals, shares and currencies fluctuate over time. The possibilities of adverse price change in future creates risk for business. Derivatives are used to reduce or eliminate price risk arising from unforeseen price change. A derivatives is a financial contract whose price depends on, or is derived from the price of another assets.

Two important derivatives are future and options

1. Commodity Future Contract:

A future contract is an agreement for buying or selling a commodity for a predetermined delivery price at a specific future time. Futures are standardized contract that are traded on organized facture exchanges that ensure performance of the contract and remove the default risk. The commodity futures have existed since the Chicago Board of Trade (CBOT) was established in 1848 to bring farmers and merchants together the major function of future market is toe transfer price risk from hedger to speculators. For example suppose a farmer who is expecting the crop of wheat to be ready in three months time, but is worried that the price of wheat may decline in this period, in order to minimize his risk, he can enter into a future contract to sell his crop in three months time at a price determined now.

Just take an another example. All we know that woolen garments demand picks up in winter season. A garment factory owner can by a factory contract of cotton to get the raw material for his products as predetermined price. This way both time is able to hedge their risk arising from a possible adverse change in the price of theirs commodity or raw material.

2. Commodity Option Contract:

Like futures, option are also financial instruments used for hedging and speculation. The commodity option holder has the right, but not the obligation to buy (or sell) a specified quantity of a commodity at specified price on or before a specified date. Option contract involve two parties – the seller of the option writes the option in favour of the buyer (holder) who pays a certain premium to the seller as a price for the option. There are two types of commodity options. A ‘call’ option gives the holder a right to buy a commodity at an agreed price, while a ‘put’ option gives the holder a right to sell a commodity at an agreed price on or before a specified date which is called expiry date.

The option holder will exercise the option only if it is beneficial to him, otherwise he will let the option lapse. Suppose a farmer buys a put option to sell 10 MT of wheat of Rs. 13000/- MT and pays a ‘premium’ of Rs. 500/- MT. If the price wheat decline, to say Rs. 1000/- MT before expiry, the farmer will the exercise his option and sell his wheat at the agreed price of Rs. 1300/- MT. However, if the market price of wheat increases by Rs. 1000/-MT, it will be better for the farmer to sell it directly in the open market at the spot price, rather than his option to sell at Rs. 13000/- MT.

Future and options trading therefore helps in hedging the price risk and also provide investment opportunity to speculators who are willing to assume risk for a possible return. Future trading and the ensuing discovery of price can help farmers to deciding which crops to grow.

Thus future and options market perform important functions that cannot be ignored in modern business environment. At the same time, it is true that too much speculative activity in essential commodities would destabilize the markets and therefore, these markets are normally regulated as per the law of the country. Commodity Options trading is not permitted in India till now.

Modern commodity exchange

To make up the loss of growth and development during the four decades of restrictive Govt. policies, FMC and the government encouraged setting up commodity exchanges using the most modern system and practices in the world. Some of the main regulatory measures imposed in the FMC include daily market to market system of margins, creation of trade guarantee fund, back office computerization for the existing single commodity exchanges , online trading for the new exchanges, demutualization for the new exchanges and one third representation of independent Directions the Board of existing Exchanges etc.

National Level Commodity Exchanges in India are:-

- NMCE : National Multi Commodity Exchange of India.

- NCDEX : National Commodity Derivatives Exchange Ltd.

- MCX : Multi Commodity Exchange of India Ltd.

- NSEL : National Stock Exchange Ltd.

NMCE: (National Multi Commodity Exchange of India Ltd It is the first demutualised electronic commodity exchange of India granted the National exchange on Govt. of India and operational since 26th Nov, 2002. The Head Office of NMCE is located in Ahmadabad. There are various commodity trades on NMCE Platform including Agro and non-agro commodities. NCDEX (National Commodity & Derivates Exchange Ltd

NCDEX is a public limited co. incorporated on April 2003 under the Companies Act 1956, It obtained its certificate for commencement of Business on May 9, 2003. It commenced its operational on Dec 15, 2003. NCDEX is located in Mumbai and currently facilitates trading in 57 commodity mainly in Agro product.

NSEL (National Spot Exchange Limited)

National Spot Exchange Limited (NSEL) is a National level Institutionalized, Electronic, Transparent Spot trading platform which commenced its live operations on 15th Oct, 2008. At present NSEL is operational in 13 states, providing delivery based spot trading of 26 commodities.

MCX Multi Commodity Exchange of India Ltd

Headquartered in Mumbai, the exchange started operation in Nov, 2003. MCX is a demutalised nation wide electronic commodity future exchange. Set up by Financial Technologies (India) Ltd. permanent recognition from government of India for facilitating online trading, clearing and settlement operations for future market across the country. MCX is well known for bullion and metal trading platform.

MCX offers futures trading in

- Metal

- Aluminium, Copper, Lead, Nickel, Sponge Iron, Steel Long (Bhavnagar), Steel Long (Govindgarh), Steel Flat, Tin, Zinc

- BULLION

- Gold, Gold HNI, Gold M, i-gold, Silver, Silver HNI, Silver

- FIBER

- Cotton L Staple, Cotton M Staple, Cotton S Staple, Cotton Yarn, Kapas

- ENERGY

- Brent Crude Oil, Crude Oil, Furnace Oil, Natural Gas, M. E. Sour Crude Oil

- SPICES

- Cardamom, Jeera, Pepper, Red Chilli

- PLANTATIONS

- Arecanut, Cashew Kernel, Coffee (Robusta), Rubber

- PULSES

- Chana, Masur, Yellow Peas

- PETROCHEMICALS

- HDPE, Polypropylene(PP), PVC

OIL & OIL SEEDS

Castor Oil, Castor Seeds, Coconut Cake, Coconut Oil, Cotton Seed, Crude Palm Oil, Groundnut Oil, Kapasia Khalli, Mustard Oil, Mustard Seed (Jaipur), Mustard Seed (Sirsa), RBD Palmolein, Refined Soy Oil, Refined Sunflower Oil, Rice Bran DOC, Rice Bran Refined Oil, Sesame Seed, Soymeal, Soy Bean, Soy Seeds

CEREALS

Maize

OTHERS

Guargum, Guar Seed, Gurchaku, Mentha Oil, Potato (Agra), Potato (Tarkeshwar), Sugar M

Regulator of commodity exchanges:

FMCL (Forward Market commission) headquarted in Mumbai, is regulation authority which is overseen by the minister of consumer affairs, food and public distribution Govt. of India, It is a statutory body set up in 1953 under the forward contract (Regulation) Act 1952.

Needs for future trading in commodities:

Commodity futures, which terms an essential component of commodity exchanges, can be broadly classified into precious metals, agriculture, energy and other metals. Current future volumes are miniscule compared to underlying spot market volumes and thus have a tremendous potential in the near future. Future trading in commodities result in transparent and fair price discovery. It reflects videos and expectations of wider section of people related to a particular commodity. It provides effective platform for price risk management for all segment of players ranging from producers, trades and processors of a commodity. It aids in improving the cropping platform for farmers, thus mimizing the losses to the farmers. It also acts as a smart investment choice in providing hedging, trading and arbitrage opportunities to market players. Historically, pricing, in Commodities future has been less volatile compared with equity and bonds, thus providing an efficient portfolio diversification option. Raw Materials form the most key element of industries. The significance of raw materials can further be strengthened by the fact that the increase in raw material cost means reduction in share prices. Industry in India a today runs the raw material price risk. Hence going forward the industry can hedge this risk by trading in commodities market.

Risk associated with commodities market:

No risk can be eliminated, but the same can be transferred to someone who can handle it better or to someone who has the appetite for risk. Commodity enterprises primarily face the following classes of risk. Namely: The price Risk, the quantity risk, the yield/output risk and the political risk, talking about the nationwide commodity exchanges, the risk of the counter party not fulfilling his obligations on due date or at any time therefore is the most common risk.

This risk is mitigated by collection of the following margins:-

- Initial margins

- Exposure margins

- Mark to Market on daily positions.

- Surveillance.

Key factors for success of commodities market:

The following are source of the key factors for the success of the commodities market:

- How can one make the business grow

- How many products are covered

- How many people participate in the Platform.

Key factors for success of commodity exchanges:

Strategy, method of execution, background of promoters, credibility of the institution, transparency of platforms, scaleable technology, robustness of settlement structure, wider participation of Hedgers, speculators and arbitragers, acceptable clearing mechanism, financial soundness and capability, covering a wide range of commodity, reach of the organization and adding value to the ground.

Basic terminologies in commodities

Arbitrage: The simultaneous purchase and sale of similar commodities in different markets to take advantage of a perceived price discrepancy.

Basis: The difference between the current cash price and the futures price of the same commodity for a given contract month.

Bear Market: A period of declining market prices.

Bull Market: A period of rising market prices.

A company or individual that executes futures and options orders on behalf of financial and commercial institutions and/or the general public.

Call Option: An option that gives the buyer the right, but not the obligation, to purchase (go "long") the underlying futures contract at the strike price on or before the expiration date of the option.

Cash (Spot) Market: A place where people buy and sell the actual (cash) commodities, i.e., grain elevator, livestock market, etc.

Commission (Brokerage) Fee: A fee charged by a broker for executing a transaction.

Convergence: A term referring to cash and futures prices tending to come together as the futures contract nears expiration.

Cross-hedging: Hedging a commodity using a different but related futures contract when there is no futures contract for the cash commodity being hedged and the cash and futures markets follow similar price trends

Daily Trading Limit: The maximum price change set by the exchange each day for a contract.

Day Traders: Speculators who take positions in futures or options contracts and liquidate them prior to the close of the same trading day.

Delivery: The transfer of the cash commodity from the seller of a futures contract to the buyer of a futures contract.

Forward (Cash) Contract: A cash contract in which a seller agrees to deliver a specific cash commodity to a buyer at a specific time in the future

Fundamental Analysis: A method of anticipating future price movement using supply and demand information.

Futures Contract: A legally binding agreement, made on the trading floor of a futures exchange, to buy or sell a commodity or financial instrument sometime in the future. Futures contracts are standardized according to the quality, quantity and delivery time and location for each commodity. The only variable is price, which is determined on an exchange trading floor.

Hedger: An individual or company owning or planning to own a cash commodity - corn, soybeans, wheat, etc. and concerned that the costs of the commodity may change before they intend to either buy or sell it in the cash market. A hedger achieves protection against changing cash prices by purchasing (selling) futures contracts of the same or similar commodity and later offsetting that position by selling (purchasing) futures contracts of the same quantity and type as the initial transaction and at the same time as the cash transaction occurs.

Hedging: The practice of offsetting the price risk inherent in any cash market position by taking an equal but opposite position in the futures market. Hedgers use the futures markets to protect their business from adverse price changes.

Margin: Margin is the percentage amount required by the exchange from the trading member for carrying out trading activities in the particular contract. The member in turn collects the margin from the client entering into trade in that contract. Though the margin amount as a whole is more significant, it can be broken into 4 kinds of margin:

- Initial Margin

- Exposure Margin

- Additional Margin

- Special Margin

Initial Margin: The amount a futures market participant must deposit into his/her margin account at the time he/she places an order to buy or sell a futures contract.

In-the-Money Option: An option having intrinsic value. A call option is in-the-money if its strike price is below the current price of the underlying futures contract. A put option is in-the-money if its strike price is above the current price of the underlying futures contract.

Intrinsic Value: The difference between the strike price and the underlying futures price for an option that is in-the-money.

Liquidate: Selling (or purchasing) futures contracts of the same delivery month purchased (or sold) during an earlier transaction or making (or taking) delivery of the cash commodity represented by the futures contract.

Long: One who has bought futures contracts or plans to own a cash commodity.

Lot Size: There are generally 2 kind of lots associated with commodity futures

Trading lot

It is the lot size in which trading activities are carried out. It means that the minimum quantity in which trading would be conducted for any particular contract of a commodity. Eg. With lot size of Crude Oil being 100 barrels, any trader / investor would have to buy / sell a minimum of 100 barrels of crude oil on the trading platform. No fractions are allowed to trade on the exchanges and the trading is carried out in multiples of lot size only.

Delivery lot

It is the minimum size for conducting delivery in the particular commodity. It can differ from the trading lot but would be always in the multiples of the trading lot. It can’t be smaller than trading lot as the delivery would not be possible in that case. Generally, the delivery lot is decided on the basis of the standards of the delivery procedure carried out in spot markets.

Maintenance Margin: A set minimum margin (per outstanding futures contract) that a customer must maintain in his margin account.

Nearby (Delivery) Month: The futures contract month closest to expiration. Also referred to as spot month.

Open Interest: The total number of futures or options contracts of a given commodity that have not yet been offset by an opposite futures or option transaction nor fulfilled by delivery of the commodity or option exercise. Each option transaction has a buyer and a seller, but for calculation of open interest only one side of the contract is counted.

Option: A contract that conveys the right, but not the obligation, to buy or sell a futures contract at a certain price for a specified time period. Only the seller (writer) of the option is obligated to perform.

Option Premium: The price of an option-the sum of money that the option buyer pays and the option seller receives for the rights granted by the option.

Out-of-the-Money Option: An option with no intrinsic value, i.e., a call whose strike price is above the current futures price or a put whose strike price is below the current futures price.

Purchasing Hedge (long hedge): Buying futures contracts to protect against a possible price increase of cash commodities that will be purchased in the future. At the time the cash commodities are bought, the open futures position is closed by selling an equal number and type of futures contracts as those that were initially purchased.

Put Option: An option that gives the option buyer the right but not the obligation to sell (go short) the underlying futures contract at the strike price on or before the expiration date of the option.

Price Limit: Price Limit is put into the place by the Exchanges on directives from FMC, the regulatory body, to keep a check on extreme price movements within a single trading session.

A price limit is defined for each commodity in percentage terms which is calculated from the previous close of the contract. If the prices hit the circuit limit on either side, the trading is halted for 15 minutes, which is often termed as cooling period. Then the trading limit gets relaxed for another 50% of the initial limit specified and margin on the contract gets increased. The revised limit is the maximum price on the higher / lower side at which trading can take place.

Different commodities have different price limits. Same commodity might be having different price limits on different exchanges but different contracts of same commodity can’t have varying price limits (in percentage terms) on same exchange

Selling Hedge (short hedge): Selling futures contracts to protect against possible declining prices of commodities that will be sold in the future. At the time the cash commodities are sold, the open futures position is closed by purchasing an equal number and type of futures contracts as those that were initially sold.

Short Position: One who has sold futures contracts or plans to sell a cash commodity. Selling futures contracts or initiating a cash forward contract sale without offsetting a particular market position.

Speculator: A market participant who tries to profit from buying and selling futures and option contracts by anticipating future price movements. Speculators assume market price risk and add liquidity and capital to the futures markets. They do not hold equal and opposite cash market risks.

Spread: The price difference between two related markets or commodities. For example, the April-August live cattle spread.

Strike Price: The price at which the futures contract underlying a call or put option can be purchased (call) or sold (put). Also called exercise price.

Symbol: Exchange provides symbol to each commodity traded on its platform. These symbols are unique within the exchange.

Symbols on MCX are quite simple and easy to identify as the name is the symbol in most cases. Eg. Gold is written as 'GOLD', Silver as 'SILVER', Copper as 'COPPER' and Crude Oil as 'CRUDEOIL' On the other hand, NCDEX has a different method of allotting symbols. Each symbol carries alphabets from the following:

- Name of the commodity

- Quality of the commodity

- Delivery centre

Technical Analysis: Anticipating future price movements using historical prices, trading volume, open interest, and other trading data to study price patterns.

Time Value: The amount of money option buyers are willing to pay for an option in the anticipation that, over time, a change in the underlying futures price will cause the option to increase in value. In general, an option premium is the sum of time value and intrinsic value. Any amount by which an option premium exceeds the option's intrinsic value can be considered time value.

Tick Size: Tick size is the minimum price movement permissible for the particular contract. It means that the minimum price fluctuation (if any) in a commodity would be the tick size. Eg. Tick Size for Wheat at NCDEX is Rs. 0.20 which means that if the wheat is quoting at Rs. 850, then the next price on the higher side should be minimum Rs. 850.2. It cannot be Rs. 850.10.

Underlying Futures Contract: The specific futures contract that can be bought or sold by exercising an option.

Volatility: A measurement of the change in price over a given time period. It is often expressed as a percentage and computed as the annualized standard deviation of percentage change in daily price.

Volume: The number of purchases or sales of a commodity futures contract made during a specified period of time, often the total transactions for one trading day.

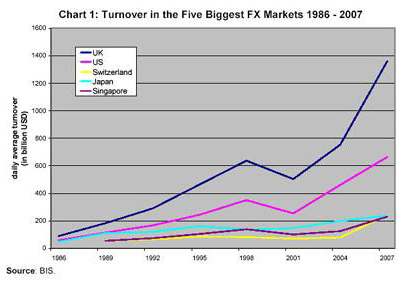

| Currency market basics: how the global currency markets work | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The currency market is the largest and most liquid financial market in the world, but also one of the least known. Currencies like the U.S. dollar, the euro and the yen trade in the foreign exchange (FX) market 24 hours a day across national borders. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Overview of the global currency markets | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

Currency in its simplest form describes the money or official means of payment in a country or region. The best known currencies include the U.S. dollar, euro, yen, British pound and Swiss franc. A commonly used currency symbol exists for many currencies, for example $, £ or €. FX markets, however, use so called ISO codes, for example USD for U.S. dollar, GBP for the British pound and EUR for the euro. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||